Bank-Insurance

Cenbank goes back to tightening loan classification rules

The Bangladesh Bank has finally reinstated its loan classification rule of 2012 by cutting the overdue time of a term loan by three months in line with the international practice in response to the condition set by the International Monetary Fund (IMF) as part of a $4.7 billion loan package.

A term loan will be treated as overdue after three months of non-payment from fixed expiry date for repayment, down from existing six months, according to Bangladesh Bank circular.

Besides, the classification period after the overdue timeframe has been kept unchanged at three months, which means a loan will be treated as default in six months after the fixed expiry date for repayment from existing nine months.

This is the first phase of the new rule which will come into effect from 30 September 2024.

In the second phase, the loan will be treated as overdue from the following day of fixed expiry date of repayment from 31 March 2025, which means the account will come under classification in three months of non-payment.

However, in another circular, the central bank addressed the pressure of rising loan costs, instructing banks not to extend instalment size of borrowers.

Banks have also been asked to extend tenure of industrial term loans and house finance taken before July 2023 to adjust the increased loan costs caused by rising lending rates.

Mustafa K Mujeri, former director general of Bangladesh Institute of Development Studies, welcomed the decision, stating that it would encourage customers to pay in instalments.

“However, the instalment amount should have been left to the bank-customer relationship. It will not work if the central intervenes in all cases. Banks should be given freedom over instalment amount and extension of loan tenure,” he added.

Emranul Huq, managing director and CEO of Dhaka Bank, said banks stand to benefit from reducing loan overdue periods.

“Extending deadlines often leads customers to delay repayments unnecessarily. Shorter loan durations facilitate quicker recovery, reduce Non-Performing Loans (NPLs), and enhance the banking sector’s liquidity,” he added.

The banker supported keeping instalment amounts unchanged, explaining that when arranging instalment payments for term loans, they consider factors such as the customer’s cash flow.

“Despite interest rate increases, our priority is to ensure that instalment payments remain manageable. If handled correctly over time and clients are financially stable, it will benefit the banking sector,” he added.

The lending rate which was capped at 9% before July 2023 surged to 13.55% in April after introducing a new lending rate formula SMART (Six-months Moving Average Rate of Treasury Bills).

Moreover, the new tight loan classification rule that was eased in 2019 is feared by the Bangladesh Bank to increase non-performing loans by around Tk80,000 crore.

The total default loan in the banking industry stood at Tk1.45 lakh crore at the end of December last year which was 9% of total loans.

Changes in loan classification over the years

Earlier in 2012, the central bank adjusted loan rules to meet IMF conditions for a $1 billion ECF program. Loans used to be classified as overdue after nine months, but under the new rules, it was shortened to three months past the repayment date.

However, the Bangladesh Bank started to deviate from the international practice gradually from 2015 through offering a special loan restructuring facility for large loan borrowers with loans above Tk500 crore. Borrowers were allowed to regularise their loans under the one time restructure program with a 12 years repayment facility at only 2% down payment.

Later, in 2019, the Bangladesh Bank eased the classification rule reinstating the provision of a nine months for treating a loan account as classified from fixed expiry repayment date.

In the same year, the central came up with a relaxed loan rescheduling policy allowing defaulters to reschedule their classified loans by making a down payment of only 2% instead of the existing 10%-50%.

However, a series of rules relaxation could not reduce default loans, rather it kept rising.

Default loans in the banking industry increased by Tk52,000 crore in five years from December 2018 to December 2023 even after rescheduling loans of Tk2,12,780 crore during this period under relaxed policies.

The Bangladesh Bank in its financial stability report published in August 2023 disclosed that the banking sector’s distressed assets including default loans, rescheduled loans and written-off loans stood at Tk3.77 lakh crore at the end of 2022.

The total distressed amount was 25.5% of total loans of Tk14.77 lakh crore according to the report.

The Bangladesh Bank for the first time disclosed the distressed assets as part of the conditions agreed with the International Monetary Fund (IMF) for the $4.7 billion loan.

Borrowers will enjoy extended repayment period to adjust rising loan costs

In another circular issued yesterday, the Bangladesh Bank said borrowers’ ability to repay loans has decreased due to higher interest rates on loans taken before July 2023. As a result, loan costs have increased based on SMART.

To address this issue, banks were asked not to increase the instalment size and adjust the increased loan cost through extending repayment tenure.

The increased amount of instalment was instructed to keep separately in a blocked account which will be not charged. Later, the amount will be split in the same size of instalment that was set before 1 July 2023, according to the circular. Such extension of repayment period will not be considered as a rescheduled loan.

Banks can transfer the money from blocked accounts soon after starting recovery, said the circular. The facility will be cancelled if any loan turns to classified despite availing the extended tenure benefit.

Only loans remaining regular based on 1 April 2024 will come under the facility, according to the circular.

Bangladesh Bank Governor Ahsan H Mansur has announced that the central bank will increase the policy rate twice within the next month to combat rising inflation. During a press briefing on Monday, Mansur said, “We will follow a contractionary monetary policy until inflation is brought under control. The policy rate will be raised next week and again next month.”

The governor expressed optimism about inflation stabilizing by March or April, although he did not specify the expected inflation rate. “While we can’t predict the exact level of inflation, we will tighten policies to bring it down. Our exchange rate remains stable, and remittances are on the rise, which should help ease inflationary pressures,” Mansur added.

Recent Rate Hike Follows a Series of Increases

On 25 August, the central bank raised the policy rate by 50 basis points, bringing it to 9% as part of its efforts to tackle high inflation. This marked the third increase in the key interest rate this year. Mansur had previously indicated that the policy rate, or repo rate, could potentially rise to 10% in phases.

Plans to Merge Smaller Islamic Banks

The governor also discussed the possibility of consolidating smaller Islamic banks. “Merging smaller banks would be beneficial. While no formal decision has been made, we are considering the option,” he said. Mansur explained that past irregularities had caused some bank owners to lose their ownership, which could make the process of consolidation easier.

He assured that depositors’ funds would be safeguarded, even if the banks are merged. “We will take actions based on the situation, but depositors’ money will be returned,” Mansur promised.

Task Force Established for Banking Sector Reform

Mansur further outlined that a task force has been formed to address issues in the banking sector, focusing on identifying distressed assets and recovering them. Initially, the task force will work with three banks, followed by an additional six. The team consists of 14 Bangladesh Bank officials, divided into three groups, with six members specifically overseeing larger Islamic banks.

Development partners will provide funding for these efforts, with external and international auditing firms assisting in the process. “Our first step will be to assess how much money has been withdrawn, both in name and covertly. If funds have been transferred abroad, we will work on bringing them back under international law,” Mansur explained.

Liquidity Support for Weaker Banks

The governor noted that some depositors were shifting their funds from weaker banks to stronger ones, creating liquidity challenges for the former. To address this, the central bank will provide funds from more liquid banks to those in need, ensuring that Bangladesh Bank covers any shortfalls if weaker banks are unable to repay.

Potential Changes in Bank Loan Targets

Mansur also mentioned the possibility of reducing the budget target for bank loans by Tk50,000 crore. This move could potentially boost private sector investment. “If we can reduce inflation to around 4%-5%, we will have the opportunity to lower interest rates,” he stated.

Bangladesh Bank (BB) has received a loan proposal totaling $2.5 billion from the World Bank (WB) and the Asian Development Bank (ADB) in several packages, aimed at supporting structural reforms, policy implementation, and investment projects.

The proposal was presented today during a meeting between Bangladesh Bank Governor Ahsan H Mansur, senior officials, and delegations from both the WB and ADB at the BB headquarters. The information was confirmed by BB spokesperson and Executive Director Husne Ara Shikha.

“The World Bank has proposed a $1 billion loan, which includes a $750 million policy-based loan requiring the central bank to implement specific policies. Additionally, a $250 million investment loan is currently in process,” said the BB spokesperson.

Similarly, the ADB has proposed a $1.5 billion policy-based loan, which will be disbursed in three phases, including a $200 million investment loan. According to the central bank spokesperson, $500 million of the loan could be received by 2025.

Additionally, a visiting US delegation, led by Brent Nieman, Assistant Secretary of the US Treasury Department, met with the central bank governor today. During the meeting, the delegation was briefed on the country’s macroeconomic conditions, though no specific loan amount was discussed by the US treasury team.

Parvez Tamal, Chairman of NRBC Bank, once known as a close ally of former Prime Minister Sheikh Hasina, has reportedly shifted his stance following the resignation of the Awami government on August 5. Tamal, who had been accused of exploiting political power for financial misdeeds during the Awami regime, is now aligning himself with student activists in a bid to protect his position.

Previously, Tamal had threatened NRBC Bank employees with termination if they supported or joined the quota reform movement. He also warned of administrative harassment for any Facebook posts or comments related to the movement. However, after the fall of the Awami government, Tamal has been providing financial support to the very student protesters he once opposed, in an attempt to distance himself from his controversial past.

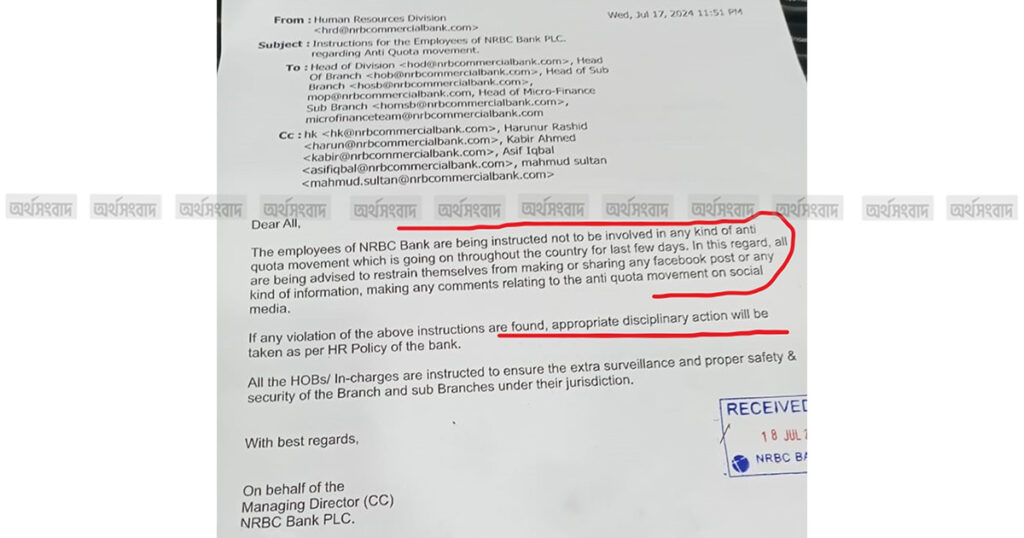

An investigation by Orthosongbad revealed that during the anti-quota movement, Tamal worked on behalf of Sheikh Hasina, even monitoring NRBC Bank staff to ensure they did not participate in the protests. On July 17, under his directive, a warning was sent to all branch managers of the bank, cautioning them about the movement. Documents related to this have surfaced during the investigation.

A directive from NRBC Bank instructed all its officers and employees to refrain from joining any assembly related to the quota reform movement or sharing any comments, posts, or information about it on social media. The email from the bank’s HR department, titled ‘C,’ warned that any violation of this order would result in administrative action in accordance with HR policies. The directive also emphasized ensuring maximum security in and around the bank and required employees to be punctual in reporting to work.

Sources suggest that NRBC Bank Chairman Parvez Tamal, in an attempt to secure his position, has been trying to win over the coordinators of the anti-discrimination student movement. This speculation gained traction after a recent event where Tamal handed over a cheque for 5 million BDT from the bank’s Corporate Social Responsibility (CSR) fund to Hasanat Abdullah, one of the coordinators of the student protests. The donation, aimed at providing treatment and rehabilitation for injured protesters, has sparked widespread criticism on social media. Many are questioning Tamal’s sudden shift, given his previous ties to former Prime Minister Sheikh Hasina and his outspoken opposition to the student movement.

At the donation event, Parvez Tamal remarked that NRBC Bank would support the dreams of those building a “new Bangladesh.” In addition to providing medical assistance to the injured, he pledged future employment opportunities and scholarships for injured students. NRBC Bank also committed to offering jobs to able-bodied members of families affected by the protests. These promises mark a stark contrast to Tamal’s previous stance, where he had vocally supported Sheikh Hasina and opposed the student protests.

Attempts to reach Hasanat Abdullah, one of the coordinators of the anti-discrimination student movement, for a comment were unsuccessful. Despite multiple calls from Orthosongbad office to his mobile phone, there was no response. Similarly, efforts to contact another coordinator, Sarjis Alam, also failed to yield any comments.

However, former law student of Dhaka University and social media figure Syed Abdullah shared his thoughts on Facebook, stating that NRBC Bank Chairman Parvez Tamal is on a mission to secure his position by ingratiating himself with the students, thereby improving his image. Abdullah urged immediate investigations by the Anti-Corruption Commission (ACC) and journalists into the activities of Tamal and his associates.

Orthosongbad made several attempts to contact NRBC Bank Chairman Parvez Tamal for comments, but no response was received.

Sources claim that Parvez Tamal, in his efforts to support the Hasina government, has distributed various donations through the bank, both publicly and covertly. Among these are scholarships in the name of Bangabandhu, a special issue of “Planet” magazine focused on Sheikh Mujibur Rahman’s life and legacy, donations to the Bangabandhu Memorial Trust, contributions to the Bangabandhu Youth Fair, and charity books and iftar events around Bangabandhu’s birthday. Additionally, the bank had provided significant funds for Sheikh Hasina’s Ashrayan Project.

Parvez Tamal, who claims to be a Russian oligarch and served as the president of the Russia Bangabandhu Parishad, has been implicated in various financial irregularities, including loan fraud, commission schemes, recruitment corruption, stock manipulation, money laundering, and the embezzlement of funds. During the tenure of former Prime Minister Sheikh Hasina, Tamal reportedly leveraged his connections with senior leaders of the Awami League to engage in these activities.

The Anti-Corruption Commission (ACC) had previously launched an investigation into Parvez Tamal, chairman of NRBC Bank, following allegations of irregular salary increases for select officials. The investigation stemmed from a complaint by a sponsor shareholder of the bank. Tamal reportedly bypassed the banking regulations, awarding significant salary increments to 27 officials while ignoring over 3,800 employees. Additionally, Tamal and his personal secretary, Asif Iqbal, allegedly pocketed excessive fees from board meetings, violating the country’s banking laws. Furthermore, the investigation revealed that Tamal had set up an unauthorized entity, NRBC Management, without approval from Bangladesh Bank. However, the investigation was abruptly halted, allegedly due to Tamal’s political influence.

In a separate case filed on July 11, 2023, the ACC accused 14 individuals, including 11 NRBC Bank officials, of money laundering and providing unlawful loans. The lawsuit alleges that the accused embezzled approximately 78 crore BDT (including interest) by issuing loans without proper collateral. Additionally, 5.97 crore BDT worth of export proceeds were reportedly laundered without being repatriated to Bangladesh. Tamal was implicated in this fraudulent activity but reportedly used his political connections to suppress the investigation.

Further details of this ongoing investigation will be disclosed in subsequent reports by Orthosongbad.